8th February 2021 | Climate | Energy

Climate transition business models; fossil energy investment is over

Welcome to Just Two Things, which I try to write daily, five days a week. Some links may also appear on my blog from time to time. Links to the main articles are in cross-heads as well as the story.

#1: Mainstreaming low carbon business

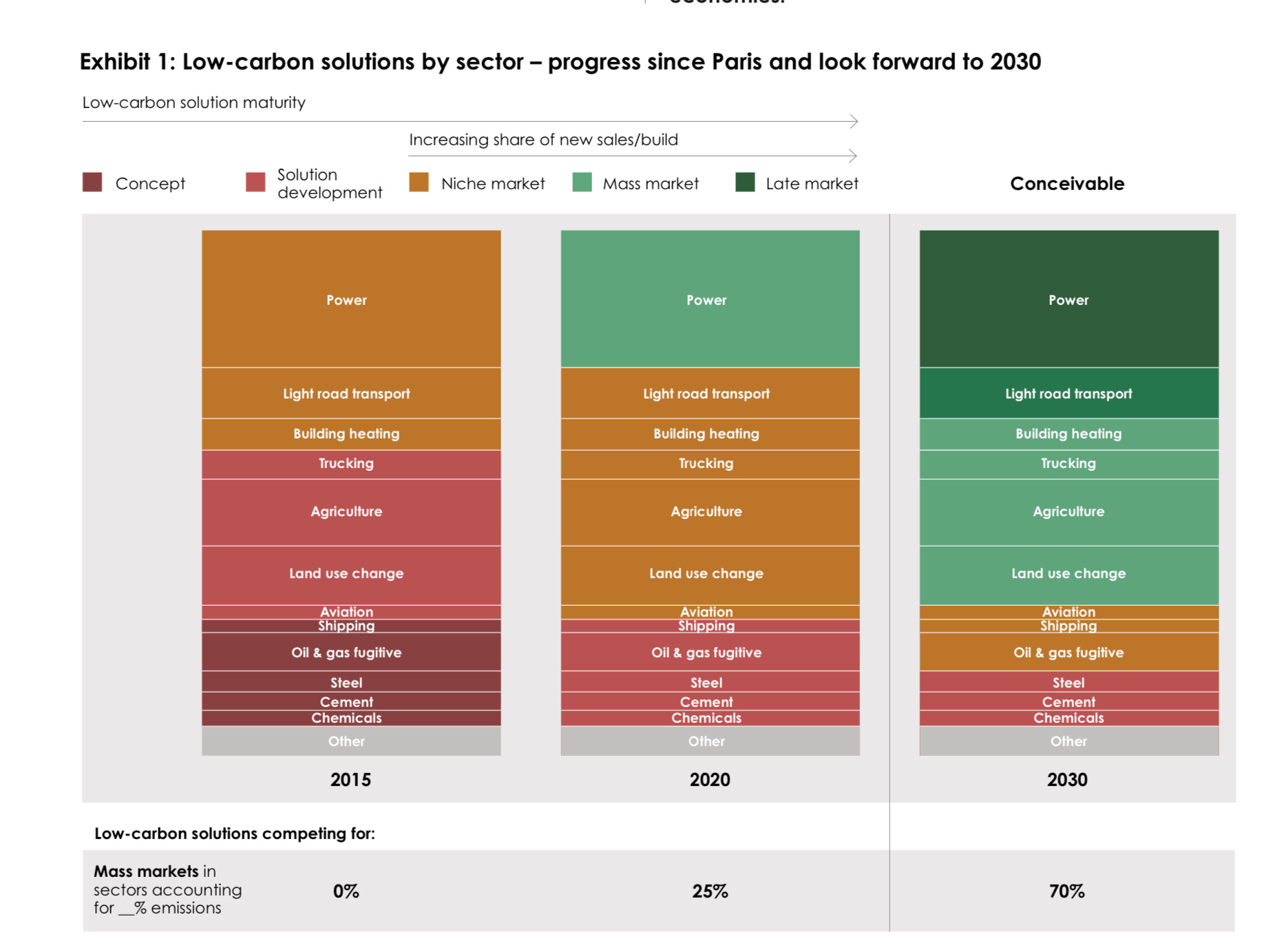

Since my piece on climate turning points I have seen a report from December that argues that the effect of the 2015 Paris Agreement is to open up 70% of the global economy to competition from low carbon solutions by 2030. The report, ‘The Paris Effect’, is from SYSTEMIQ. This is the money shot:

So, to spell it out, in 2015, when the Paris Agreement was signed, no business sector saw effective competition from low carbon solutions. By 2030 more than two-thirds of the economy—according to their analysis—will see mainstream low-carbon market solutions.

The colour coding combines some light Technology Readiness Levels analysis to market diffusion. Concepts are at the bottom, through to pilots or demonstrators, and then through niche sector take-up to full market diffusion.

The 2015 Paris Agreement, it argues, created clear political agreement about the direction of travel, creating the confidence to make clear policy signals. These are now maturing:

The report highlights that the state of the macroeconomy today further improves the conditions for a shift to a low-carbon economy. Ultra-low interest rates are well suited to clean technologies, with a higher proportion of costs up-front. The growth of digitisation also supports an expansion of resource-efficient, ‘as a service’ business models. And the economic effects of Covid-19 have overturned a lot of assumptions about how we live with implications for transport, and our consumer spending habits.

However, the transition is not assured and governments have a key role to play. Part of this will take the form of direct support… In addition to de-risking the positives, there’s a strong push for climate transparency.

One conclusion: it takes 15 years for industry supply chains and production technologies to adjust to a regulatory push—even when intentions are good—because they are complex systems with strong habits of knowledge and high levels of technical lock-in.

(H/t Ian Christie)

#2: Fossil energy investment is over

My news feeds are full of stories that all say the same thing: the business case for new fossil fuel investments is over. Here’s some examples of that.

President Biden announced plans to stop drilling for oil and gas on federal land.

As the President of the European Investment Bank, Werner Hoyer, announced its 2020 results he said that “To put it mildly, gas is over.” It will stop funding for large-scale heat production based on unabated oil, natural gas, coal or peat, upstream oil and gas production or traditional gas infrastructure by 1 January 2021.

No major oil company bought any of the recent oil leases offered in the Arctic refuge in Alaska. The only significant bidder was Alaska's state-owned economic development corporation.

New York State, and its pension funds, has announced plans to divest from oil and gas stocks—the first US state to do so.

The same article quoted CNBC ‘Mad Money’ host Jim Cramer as announcing in 2020 that he was “done with fossil fuel” stocks… He told listeners, “My job is to help you try to make money… And the honest truth is I don’t think I can help you make money in the oil and gas stocks anymore.”

Substantial Mozambique coal assets were sold for a dollar.

Three European banks have committed to stop financing the trade of oil from Ecuador’s Amazon region.

One of the few outliers is the controversial approval in the UK for a deep mine that has permission to run to 2049. It would produce coking coke for use in steel production. Justin Pickard on Twitter noted “the bad international & environmental optics of continuing to have a steel industry.”

Of course, reducing new investment on its own is not enough. There’s still a lot of legacy coal and gas production out there. Carbon pricing will nudge demand down, and one of the early straws from the Biden administration, according to the Financial Times, is that the carbon price might be pushed up as high as $100 per tonne by 2030. The Lex column (paywalled) summed this up:

The $100 price would be more than four times the average figure employed internally by companies using carbon pricing to manage risks and reduce emissions, according to CDP, a non-profit. It is 10 times higher than the 2019 global average of governments’ pricing initiatives…

A $100 price would supercharge investment in low-carbon technologies but it would also cripple businesses that could not adapt or secure government support. About $2.1tn, or 3.7 per cent, might be wiped off the market capitalisations of the 1,000 largest listed companies globally, according to calculations for Lex by consultancy Planetrics, part of Vivid Economics.

The 100 least resilient companies would lose just under half their market value. The best performing 100 would rise by 28 per cent.

But we still need to do more. One of the more interesting proposals is an international agreement to leave the oil in the ground, based on similar mechanisms that underpin the recent Treaty for the Prohibition of Nuclear Weapons. There’s more on this idea in Le Monde Diplo, in English. The idea has the support of the former Irish President Mary Robinson, among others.

Events: Edinburgh Futurists is holding a free meeting tomorrow, Tuesday 9th, talking to Paul Collier about his book Greed Is Dead, co-written with John Kay, on “politics after individualism”. It starts at 18.30 GMT. Sign up is here.

j2t#026

If you are enjoying Just Two Things, please do send it on to a friend or colleague.