25 July 2023. Scenarios | Finance

The ‘long boom’ that wasn’t // The next economic crisis will be caused by the climate crisis [#480]

Welcome to Just Two Things, which I try to publish three days a week. Some links may also appear on my blog from time to time. Links to the main articles are in cross-heads as well as the story. A reminder that if you don’t see Just Two Things in your inbox, it might have been routed to your spam filter. Comments are open.

Apologies for the slower publication schedule. It’s been a busy time at work.

1: The ‘long boom’ that wasn’t

I spent much of the ‘90s working in a technology-related job, launching an interactive television channel for a cable company in London. One of the side effects of this was that I needed to know about the nascent internet, and to do this you needed to read WIRED magazine. At the time, this was like opening a vein and injecting yourself with Silicon Valley, before it became a vampire.

And, because Peter Schwartz of Global Business Network was more or less the resident futurist of WIRED magazine, I would end up reading a lot about what I now know was a narrow view of what futures did, and why it did it.

Obviously WIRED has long since lost the cachet it had then, when Kevin Kelly edited it and it hadn’t yet been acquired by a global publishing company. All the same, it has been a surprise to find quite a lot of the people I follow pointing to a long post by Dave Karpf about one of Wired’s most notorious futures articles, on its 25th anniversary. The article jarred at the time.

The cover story, by Peter Schwartz and Peter Leyden, was called ‘The Long Boom’, and it later spawned a book. The article itself is still on the Wired site, but available only to subscribers.

But the book blurb gives you enough of a sense of the argument:

Analyzing economic, political, technological and socio-cultural trends that began to converge in the early 1980s, the authors offer a compelling — and highly plausible — vision of how the next twenty years will unfold. By 2020, we can expect to experience tremendous advances in now-emerging technologies; widespread adoption of alternative energy sources; increased productivity; and, perhaps most important, the creation of a truly global economy.

Anyway, it’s fair to say that looking back at it 25 years on, Dave Karpf hates the article. He takes an axe to it, at least metaphorically. It seems that, for whatever reason, Karpf has been working his way through the 1990s Wired archive. This is his general conclusion:

I run into a lot of incorrect predictions as I read through the WIRED archive. 90s WIRED was chock full of a very particular style of futurism — one that has, uh, not aged especially well... The thing that sets me back on my heels, though, is that a lot of those old WIRED techno-optimists are still out there making predictions today. And, to hear them tell it, they were right all along.

The Long Boom was a single scenario — and we’ll let it pass for now that the whole point of scenarios is that they travel in sets of three or four, because they are supposed to characterise a range of divergent possible futures.

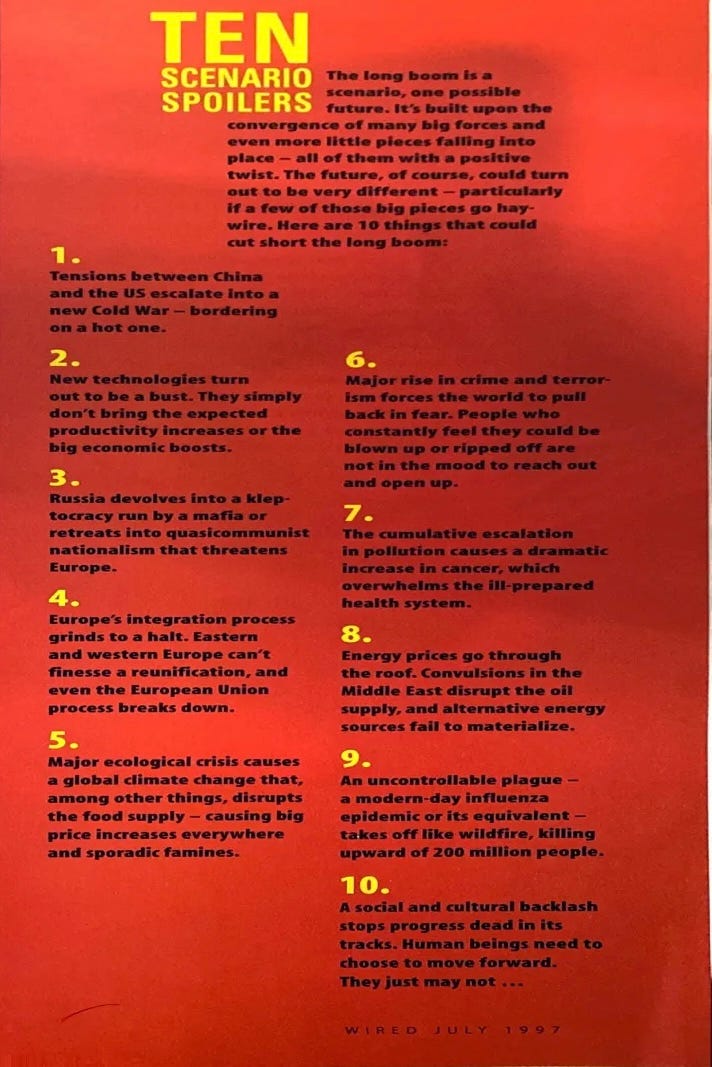

The way the original WIRED article covered this off was by listing ten things that might throw this Elysian future off-course. Karpf includes this page as an image.

It’s not a great image, but about half of these things have happened, perhaps more. America and China are engaged in a Cold War; the technologies haven’t ushered in a new wave of productivity; Russia is a kleptocracy; there is a serious climate crisis; we have had a global pandemic.

And, of course, in a proper set of scenarios, some of these possible future elements would have been included in different ways in the other scenarios in the set. Futurists aren’t supposed to bet it all on black. By doing that, they have turned it into a prediction or a forecast.

Part of Karpf’s complaint is just about the politics of this long boom scenario:

The world they are invoking is one where (1) neoliberalism spread everywhere, and works great, (2) its benefits are widely distributed, (3) scientific and technological breakthroughs become easier and faster with time, and (4) on balance, none of those scientific or technological breakthroughs are used for harm. This is… not the world we inhabit today. The neoliberal economic order has not lived up to its billing... I have to imagine that if we could transport the 1997 versions of Peters Leyden and Schwartz to the present-day United States, they would be awestruck reading Twitter on an iPhone and then appalled by the news items they encountered.

A second part of Karpf’s complaint is that in the face of the evidence that things didn’t quite work out like he expected, Peter Leyden has more or less doubled down, in an article published last year, called ‘The Great Progression’. Of those 10 problems, Leyden writes:

All 10 did actually appear in some form over the course of those 25 years (including a global pandemic), but the remarkable thing is that they still did not stop the overarching story.

About which Karpf has this to say:

Most people read those 10 spoilers and say “haha, so cursed. All of these happened. No wonder the world is such a mess.” Long Boom co-author Peter Leyden looks back at his 25-year-old preditions, spoilers and all, and declares (paraphrasing) "Yup. Nailed it. The spoilers didn’t even matter. Nothing could stop the Long Boom.”.. Let me say this again: If you retrofit your predictions to insist they were right after all, you will never learn a single damn thing.

Karpf finishes his piece with a long take, or maybe a take-down, of technological optimism, and I’ll just pull one quote from that which I think sums up the problem with the ‘Long Boom’ as a piece of future work:

This ideological commitment to optimism means the authors don’t begin from the data and trends, then arrive at optimistic conclusions. Instead, they begin with the rose-colored glasses and develop a “scenario” of how everything is poised to turn out great. (Scenarios like this are really just predictions with built-in plausible deniability. This kind of scenario is just a prediction clad in fake mustache and jaunty hat.)

I’ll probably borrow the idea of ‘jaunty hat’ futures as a critique of a certain type of futures work. Looking back, ‘The Long Boom’ tells us a couple of things about the history of that whole strand of business futures that Global Business Network came to exemplify in the 1990s. The first is that it had no critique of power, and the way that power plays out in processes of change. I think I knew this at the time.

The second, which I only understood much later, was that ‘The Long Boom’ probably represented the high water mark of that kind of empty business futures. Everything in that particular futures tradition since then has been historical footnotes. That WIRED cover was a marker that it had run out of steam.

2: The next economic crisis will be caused by the climate crisis

I wrote here recently about arguments that economics and financial models were understating climare risk. It seems that I need to come back to this, since Creon Butler, at Chatham House, has a persuasive article that says that climate change will be the source of the next financial crisis. (Disclosure: I work with Chatham House from time to time).

This might seem obvious to most Just Two Things readers, but it doesn’t seem to be obvious to the financial community. So I’ll let him spell it out:

The likely trajectory of climate change, given current global performance on emissions reduction, has been spelled out repeatedly . Extreme weather events, like the unprecedented heatwaves suffered by Southern Europe, the US and China this week, will become even more frequent and destructive as a result... Crop failure will lead to much higher food prices and millions of economic refugees . Prime real estate and agricultural land in coastal areas will be abandoned in the face of repeated flooding.

Carbon-dependent industries will face sudden closure as public opinion and government regulation shifts, while other sectors will suffer potentially devastating supply chain breakdowns. New diseases and disease patterns will impose heavy costs on public budgets.

(Wildfire in Spain, 2023. Sergio Torres. CC BY-SA 4.0. Via Catalyst.cm)

There was a time that these might have been treated as ‘uncertainties’. Butler’s not having any of this:

In many cases they are now inevitable, even if mitigation policies accelerate radically.

But so far, none of this has had any meaningful effect on asset prices, except, marginally, around the edges. This is despite relatively credible actors (for the finance sector) such as central banks making some of these points quite noisily. Butler suggests that there are several reasons for this.

Financial markets in the US and the UK are prone to what I’d call (though he doesn’t) magic bullet thinking about technology and climate change, that somehow we’ll get to a tech fix just in time. This might be because they spend too much time hanging out with Silicon Valley types who are over-confident about technology and not nearly pessimistic enough about climate change. (To be clear, this last bit is my gloss on his argument).

This is amplified because the people in financial markets think that climate change can’t be a problem because it’s not being reflected in markets yet. Obviously this is weirdly recursive argument that puts too much faith in markets. As Butler says:

(T)his view assumes that markets are rational, accumulating and then reflecting all available information. It also assumes away the enormous challenges – both technical and financial – in diffusing new technologies rapidly around the world.

Markets are inherently short-termist. So climate change seems complex and far enough away to be thought of as uncertain, whereas topical concerns such as inflation and increasing public debt crowd in on their day-to-day thinking.

It takes time for asset prices to catch up with underlying fundamentals, and in the meantime there’s quite a lot of crowd-based groupthink.

As a result, the mismatch between the asset price and an objective assessment of underlying value persists, or even gets worse.

As we saw in the run up to the global financial crisis, investors who saw what was coming and shorted the market were at the edge of the finance world and typically regarded with scorn—to the point where it was sometimes hard for them even to place their trades. (This is more or less where Michael Lewis’ book The Big Short starts.) And so it’s hard to puncture the groupthink.

This isn’t the only way that markets behave unreliably:

(H)ydrocarbon-based industries use political lobbying to delay or weaken regulatory measures that threaten their legacy businesses, even when there is an overwhelming economic rationale for the change.

Investors are creatures of habit. They tend to believe that the past will be the most reliable guide to the future, despite having to publish advertising which requires them to remind their customers that this may not be the case.

And frankly, Butler finds all of this a bit surprising:

It is striking that these factors are still so significant despite all the effort that has gone into sensitizing financial institutions to the need to understand, measure and be transparent about the climate risk in their portfolios since Mark Carney’s 2015 speech highlighting the issue. Whatever the reasons for the markets’ current equanimity on climate risks, a sharp adjustment looks increasingly probable. The longer it is delayed, the sharper it is likely to be – and the more potential triggers emerge.

So how will this crisis happen? There is a surprising number of ways, which leads one to think that the crisis might be “overdetermined”.

One way is that analysts and regulators start using better models to assess financial risk in their stress tests, which means that portfolios will need to adjust. While it’s unlikely that either analysts or regulators would intentionally create a financial crisis, they have different incentives within the system from investors, and significant adjustments can have unintended effects and unintended outcomes.

Another way is that the property and insurance market could contract as a result of climate effects, especially in areas where there is a lot of property at risk of climate change (Miami, Shanghai) in places where the property market is already over-leveraged (i.e. it is carrying too much debt and/or risk).

(Simulated view of South Beach, Miami if global temperatures rise by 2 degrees Celcius. Image: Nickolay Lamm, courtesy of Climate Central/ sealevel.climatecentral.org, via Archinect)

We’ve seen signs of this with insurance companies pulling out of California, meaning that buildings are harder to insure, which means that their value falls. Which can create tipping points in balance sheets.

Third, climate risk could limit the access of countries in the global South to international finance, leading to debt default.

Or fourth, as climate change risks become more visible (see: wildfires) public opinion starts demanding more aggressive political and regulatory action on climate. This might lead, for example, to effective carbon prices that change business models and asset values of businesses that are more exposed to climate change.

Butler makes a related point here about the global political negotiations around climate change, which could also trigger rapid re-assessments of climate risk:

For example, if the Bridgetown Initiative and Summit for a New Global Financing Pact fail to shift positions in the G20, markets may conclude there is no realistic chance of closing the massive climate finance gap (estimated at $3tn per year) required to deliver net zero.

As the saying goes, even if you’re not interested in climate change, climate change is interested in you. And our choices around climate change largely come down to whether we manage the crisis or whether we don’t. Managing is better. As Butler says:

(I)t would be far preferable if economic policymakers across all parts of government recognized that they cannot afford to put this threat to one side, even when faced with the parallel challenges of high inflation, rising debt and low productivity. The climate threat has to be tackled simultaneously with these other challenges. Indeed if one is forced to choose, the climate threat should be the economic policy priority.

j2t#480

If you are enjoying Just Two Things, please do send it on to a friend or colleague.