Welcome to Just Two Things, which I try to publish daily, five days a week. Some links may also appear on my blog from time to time. Links to the main articles are in cross-heads as well as the story.

#1: Putting complexity back into economics

The economist Brian Arthur has an article in Nature on the emerging discipline of “complexity economics”. Arthur, who led the Santa Fe Institute’s research programme on complexity in economics for many years, was the economist who identified that it was possible to have increasing returns to scale. He’s also the author of a well-regarded book on technology innovation.

(Brian Arthur)

It’s quite a long article, but it is not technical, and it is clearly written. In particular it takes care to spell out the differences between neo-classical (or “equilibrium”) economics and complexity economics as explanatory models of actual behaviour:

Complexity economics sees the economy — or the parts of it that interest us — as not necessarily in equilibrium, its decision makers (or agents) as not super-rational, the problems they face as not necessarily well-defined and the economy not as a perfectly humming machine but as an ever-changing ecology of beliefs, organizing principles and behaviours.

I probably don’t need to rehearse the limits of neoclassical or conventional economics here, with its assumptions of rational actors with full information, and markets that seek equilibrium, assumptions that also simplify analysis, especially mathematical analysis. But it’s not a good description of actors under conditions of uncertainty:

Companies in a novel market may have different technologies, different motivations and different resources, and they may not know who their competitors will be or, indeed, how they will think. They are subject to what economists call fundamental uncertainty... It follows that rational behaviour is not well-defined. Therefore, there is no ‘optimal’ set of moves, no optimal behaviour. Faced with this — with fundamental uncertainty, ill-defined problems and undefined rationality — standard economics understandably comes to a halt.

Down the years some distinguished economists have pointed this out. And when you model behaviours under these conditions, the outcomes start to look much more like ecologies:

The overall scene looks like species competition in palaeozoological times. Such outcomes are common with complexity in the economy. What constitutes a ‘solution’ — the outcome of the model — is frequently an ecology in which strategies, or actions, or forecasts compete; an ecology that might never settle down, and that shows properties that can be studied qualitatively and statistically.

Alfred Marshall suggested in the 1890s that economists should be trying to create a form of “economic biology”. It seems it might have served them better than physics envy.

Arthur observes that this work is only worthwhile if if produces better explanations of how the world works in practice. But three elements that emerge from this model are worth noting:

In complex systems, information is often channelled via networks, and the quality of networks matter. Sparsely populated networks behave very differently to dense ones. This also means that time matters.

Networks have the potential to create cascades of information, and exhibit power law effects. In turn this means that long-tail distributions of outcomes are likely. (Events at the extreme ends of distributions are more likely, as the financial sector discovered after the financial crisis).

The combination of complex systems and network effects means that systemic risk becomes a property of the system.

One of the implications of all of this is that different policy approaches are required. In “equilibrium economics”, policy usually involves adjusting incentives. In “complexity economics”, it assumes that new behaviours are more likely to emerge and parts of the system become open to capture by players who can game the system successfully.

Arthur mentions the Russian transition from communism, the deregulation in 2000 of the Californian energy market, and the light touch regulation of Wall Street, pre-2008 crash. Each of these systems was first gamed, and then crashed. None were well explained by existing models. We need better understanding of how such systems work, and where weaknesses develop, to inform better policy.

I was also struck that the paper appeared in Nature rather than an economics journal. It wouldn’t surprise me if bypassing the economics journals was a deliberate strategy, since they tend to be a source of conservatism in the discipline, not of innovation.

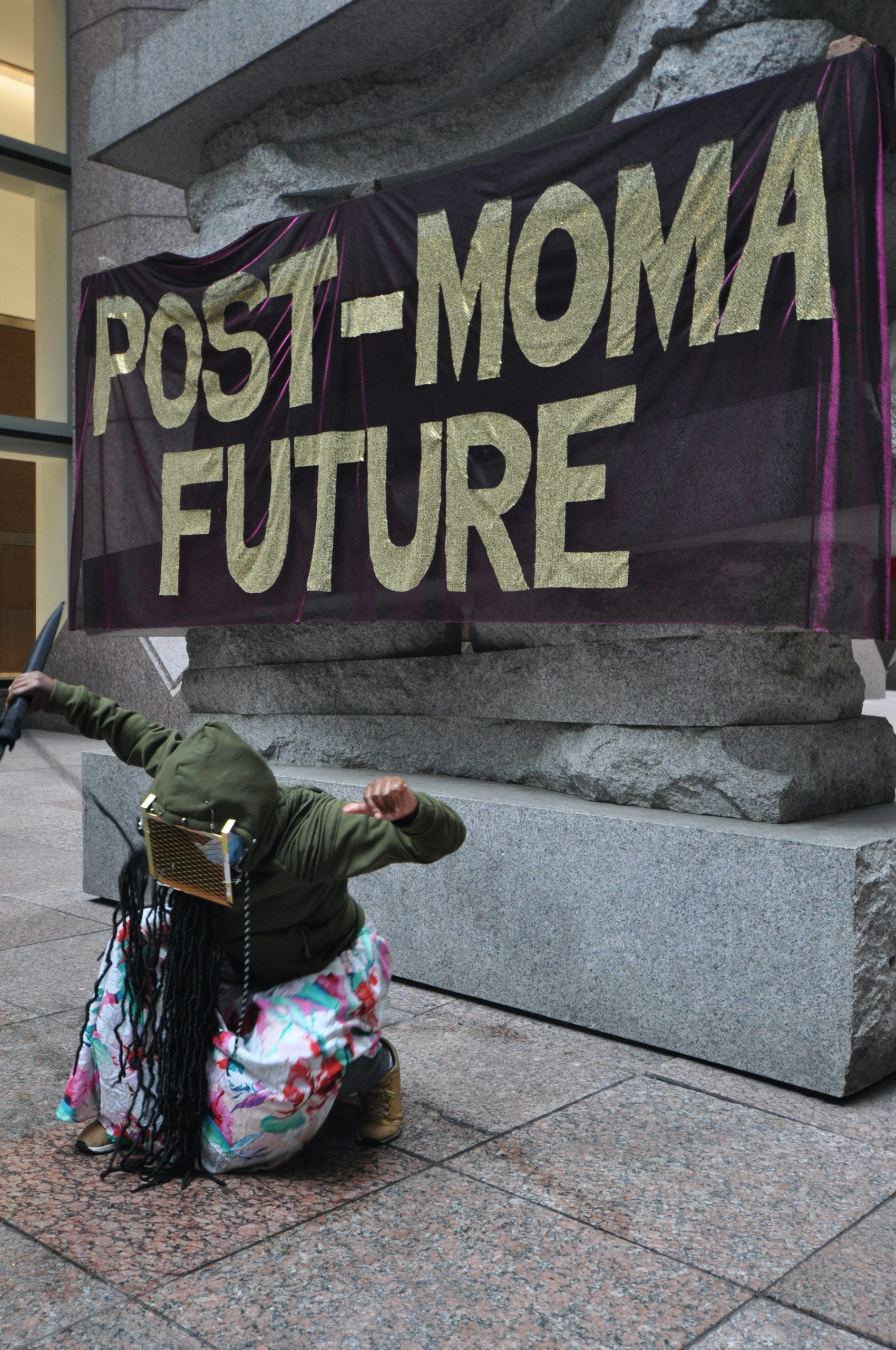

I’ve been trying to work out what to make of ‘Strike MOMA,’ a ten-week campaign of street art events outside of New York’s MOMA that is designed to draw attention to some of the material ways in which the Museum is run—and who gets to run it. The online magazine Hyperallergic has the best coverage.

(Source: Hyperallergic)

The action has clearly got MOMA rattled. A letter from the Director, Glenn Lowry, went out of its way to misrepresent the protests, as Hyperallergic’s editor-in-chief documented. A poet who was due to read at a MOMA online event was asked to submit his poems for review in advance; his response was to withdraw from the reading and read his work outside as part of the Strike MOMA event instead.

The Strike MOMA activists have produced a manifesto, although it is overly academic. Its letter to MOMA staff is a more accessible version:

By now, you probably already heard that the board of trustees of MoMA who run this museum are all getting rich off of building the prisons that lock our people up, building the concentration camps that lock up our undocumented family and separate children from their mothers. You heard that there are board members who get rich selling guns, bombs, war planes, and surveillance technology to use against our people back home in the countries we come from the same way they sell weapons to the NYPD... We come to demand a new MoMA. We gotta fight back and this is the only place where we can touch these fools.

MOMA’s also made missteps. The former chair, Leon Black, stepped down from the role over his previous associations with Jeffrey Epstein, but remains on the board.

The artists organising the event aren’t proposing an alternative model, but sometimes calling a thing by name is enough work for one moment. As Hyperallergic editor-in chief Hrag Vartinian observes,

Strike MoMA does not talk about destroying the museum, but about taking “care of art that isn’t linked to the monsters that destroy us.”... these art behemoths... continue to pretend they are about upholding quality rather than the money, power, tastes, and world views of billionaires and their courtiers.

Part of our current moment is about the power and influence of billionaires who have benefitted from deregulation, financialisation, lower taxes, and bailouts in the years since the 80s, the ways in which they maintain their wealth, and the effects that this has on the structures of our society—even the structures of feeling in our society. It’s clearly connected to ideas about decolonisation.

This isn’t the first time billionaire art donors have been critiqued: the co-chair of the Whitney, Warren Kanders, stepped down in 2019 after Hyperallergic reported that the tear gas his company makes had been fired at migrants on the Mexican border. He complained about the “toxic” atmosphere around wealthy donors, which seemed to miss the point.

What’s new, I think, about the MOMA protests, is that they aren’t aimed at an individual. They’re aimed at the whole model of how elite art institutions are run.

j2t#083

If you are enjoying Just Two Things, please do send it on to a friend or colleague.