21 March 2022. Capitalism | AI

Welcome to the new world of asset manager capitalism. Pointing machine learning at poetry.

Welcome to Just Two Things, which I try to publish daily, five days a week. Some links may also appear on my blog from time to time. Links to the main articles are in cross-heads as well as the story. Recent editions are archived and searchable on Wordpress.

1: Welcome to the new world of asset manager capitalism. We’re all working for Blackrock now.

In the UK it’s the week of the Chancellor’s spring statement, once known as the Budget, and a moderately big deal. So I’m going to have two or three economics pieces mixed in this week.

The first of these pieces is an argument that we’ve moved into a new form of capitalism—“asset manager capitalism”—in which the bulk of ownership of corporations is held by a tiny number of asset managers—Blackrock, Vanguard, State Street, and a few others. This argument is made by Benjamin Braun in a paper published last year. In this account I’m drawing on a recent blog post by the indefatigable Cory Doctorow.

These funds are giant. Between them, they own an average of 22% of every S&P 500 company. They don't just own a big stake in a whole sector – like Warren Buffet buying a big chunk of all four airlines. They own significant stakes in every industry – not just airlines, but hotels, resorts, rental car agencies, etc.

But although the pools of funds they command are vast, they are mostly acting on behalf of other investors—pension funds and so on—and the deal that their customers expect is that in general they represent the stock market and bond market, they track them so they follow the overall market (they are usually ‘index funds’) and because they are index funds, they charge the lowest possible fees. There is no ‘decision’ involved in being an index fund: you follow the market indices.

So although their scale ought to give them power, it doesn’t.

(Source: Braun et al. Here.)

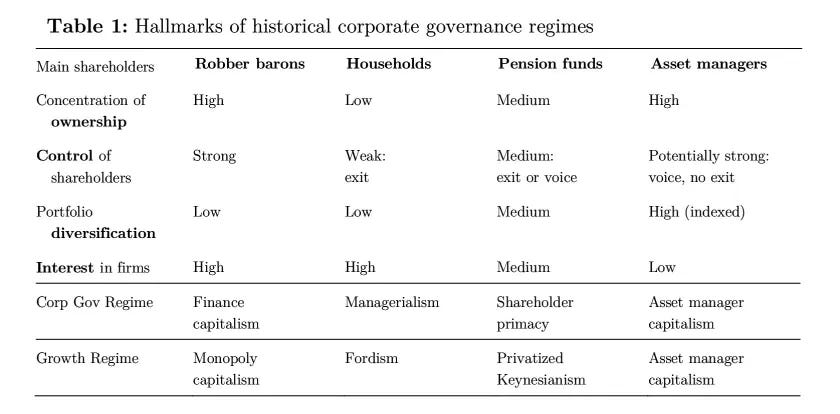

Doctorow shares a table from the original article that maps a kind of history of corporate ownership over the last century or so—going back to ‘robber barons’ and then working forwards through the post-war managerial capitalism and the later 20th century shareholder capitalism.

And this table suggests that this ownership structure—the current asset manager capitalism—is super-imposed on the corporate governance and incentive structures that were designed for post-Milton Friedman shareholder capitalism.

So we’ve moved on from an era where a lot of corporate behaviour was actually driven by short-term finance-driven incentives—and destroyed a lot of productive value in the process. Now, in practice, our vast super-investor asset managers are just following the market—or having an algorithm do it for them.

the shareholderism era was dominated by too much voting: pension fund managers and other "activist" investors demanded that companies produce short term gains on threat of mass investor exits, which would tank the share price and beggar the company executives.

On the face of it, Asset Manager Capitalism could give us the best of both worlds. Asset managers are the very definition of long term, "patient capital" because they can't sell their shares. And since they've got these incredible economies of scale, it's worth their while to pay experts to track and intervene in corporate governance.

Cory Doctorow doesn’t say this, but the reason it should be worth the while of asset managers to track and improve corporate governance is that—if you can’t sell up—it’s one of the few things that is likely to improve corporate performance and corporate outcomes.

But: they don’t. Hardly at all. Almost never:

In fact, Big Three managers are the King Logs of corporate governance. Between 2008-17, 4,000 shareholder proposals were tracked by the Russell 3000 index. None of them came from a Big Three asset manager.... For all that Blackrock's Larry Fink talks a big game about environmental sustainability, Blackrock is more likely to vote against ESG resolutions than other shareholders.

One of the quirks of having large asset management vehicles own or control so much of the value of shareholdings across so much of the economy is that it creates disincentives to collude on price. If you just control the airline sector, driving up prices is a good idea. If you control the airline sector, and the hotel sector, and the hire car sector, pushing up airline prices kills the other two sectors. It’s not in your interest:

Writing about this for NY Magazine, Eric Levitz cites Matt Bruenig, who calls it "market socialism." Asset Manager Capitalism has delivered low prices while "rationally planning" not just a single industry, but all the industries.

Well, obviously the ‘socialism’ part of this needs to be taken with a huge pinch of salt. Because actually the people who benefit from the work of the big asset managers tend still to be the people who are likely to be more wealthy, in higher paying stable jobs, and so on. Their end-beneficiaries represent a sub-section of the total population, even within the world’s richer countries.

I clearly need to go back to Braun’s paper and read it properly. But the economics of asset manager capitalism are interesting. Doctorow suggests, on the basis of various experts, that asset managers prefer low interest rates to higher interest rates (they encourage savers into chasing investments that give them better returns than they get from banks) and that they also prefer lower wages. Asset inflation (also a function of low interest rates) are good for existing wealth holders, and terrible for intergenerational equity.

And there’s a further twist to this: if you’re sitting in the shoes of (say) Blackrock, you’re going to make more money from influencing the central banks, on things like interest rates, than you are going line by line through the governance proposals of hundreds of companies.

But even if we don’t fully understand what it means yet, changes in the models of capitalism are inherently interesting:

Levitz says "Understanding contemporary capitalism requires paying as much attention to its novel oddities as to its myriad continuities."

I was reminded, though, of a conversation I had with a former Hungarian colleague. She’d worked in public policy roles before she joined the consulting business I then worked for, which mostly worked with private sector clients. One day I asked her what her impression was of our commercial sector clients. “Their decision-making and their layers of management”, she said, “remind me of the Soviet era businesses in Eastern Europe.” Perhaps that’s what’s meant by “market socialism”.

2: Using machine learning to illustrate Emily Dickson

The journalist Clive Thompson decided to set loose a machine learning program on doing some images for poem by the 19th century poet Emily Dickinson that he particularly liked. The verdict: quite good, but not that good.

The article is on Medium, with its slightly restrictive paywall.

Thompson chose Emily Dickinson because he likes her work and because it is highly metaphorical. Specifically he chose her poem ‘Because I could not stop for death’, which you can read here. It is a favourite of his. (He may also have chosen her because she’s out of copyright.)

He chose to do AI art because he’s been intrigued by the idea since he read some pieces about how that particular AI sub-genre is coming along.

And then he fed Emily Dickson’s poem into an AI generator software ‘Dream’, line by line, or more precisely, couplet by couplet. The article goes through the art the program created for each couplet.

Dream lets you pick from several different visual styles to guide the AI’s drawing. I chose three — “Steampunk”, “Synthwave”, and “Fantasy Art” — to illustrate each couplet, so we’d get three different attempts at visualizing each couplet. Those three styles seemed pretty appropriate because I’ve always thought that collections of Dickinson’s poetry should be illustrated like novels from the golden age of sci-fi.

Well, if you want to follow this couplet by couplet, you should go to the Medium piece, but here’s an extract:

We passed the Fields of Gazing Grain —

We passed the Setting Sun —

...produced this image:

(Source: Clive Thompson)

Thompson’s commentary:

These pretty clearly show fields of grain and a setting sun. The second and third image processors clearly share some aesthetics, since they both hit upon the big floating vertical lines too, a sort of sky-born echo of the grain. Again, though, nothing of the poetic dimensions of the language really finds it way into the images. These fields of grain aren’t “gazing”.

And his general conclusion is that this is all a bit dull:

All told, I think the AI did a cool but not terribly interesting job of illustrating the poem. The main problem is the AI’s bluntly literal nature. It doesn’t seem to have any ability to grok the metaphors at hand.

Maybe we shouldn’t expect too much here, since as Thompson observes, plenty of humans have problems grasping metaphor as well. He’s going to try some more experiments, and clearly had a good time playing with the software. But it does suggest that AI (or more exactly, machine learning) is going to have to do quite a lot more work before it achieves consciousness. Or whatever large claims are currently being made for it in Silicon Valley and elsewhere.

Ukraine notes:

With the arrival of Syrian troops in the war in Ukraine, as Assad repays his debt to Russia, comes—in its mirror image—uncomfortable questions about the difference between Ukrainian refugees and Syrian refugees. Not to labour the point, but both have had their cities shelled by Russian artillery.

In The New Humanitarian, ‘Ibrahim’ writes:

Crossing the Polish-Belarusian border reminded me of fleeing Syria in 2019. The fear I felt was very similar to the difficult days we went through during the war. My family was displaced from our town outside Damascus when the Syrian revolution turned into a civil war. We lived under siege for two years. My younger brother was killed by shelling... The media and journalists should know how to talk about migration and humanitarian crises, but even they are dividing people by the colour of their eyes and skin. Why are bombs falling on Ukraine more important than bombs falling on Syria?

My former colleague Mouna Kalla-Sacranie makes a related point in the online magazine Gal-Dem. She is Palestinian, and notes that some of the footage that has surfaced online tagged as if is from Ukraine actually comes from material shot in occupied Palestine. As she says, this is interesting for two reasons:

Firstly, it exposes that when images of Palestinian suffering and bravery are co-opted and extracted from their true context, people respond with an empathy and outrage that the Palestinian cause is rarely afforded. Secondly, it reveals an interesting and uncomfortable parallel between the two regions – a parallel that many Western correspondents are either reluctant to acknowledge, or have previously dismissed as being divisive and far-fetched.

I’m not going to speak for Mouna—she is well able to do that for herself. But as with Ibrahim’s piece above, it’s clear that the war in Ukraine makes some fault-lines very visible.

——————————-

j2t#283

If you are enjoying Just Two Things, please do send it on to a friend or colleague.