1 March 2022. Sanctions | Poetry

Central banks become ‘legitimate targets’. During the war—reading Ilya Kaminsky

Welcome to Just Two Things, which I try to publish daily, five days a week. Some links may also appear on my blog from time to time. Links to the main articles are in cross-heads as well as the story. Recent editions are archived and searchable on Wordpress.

1: Central banks become ‘legitimate targets’

The general view in the literature is that economic sanctions are not particularly effective, and that—to the extent they are effective—they hurt the poor more than the rich.

But mostly such sanctions have been directed against less affluent countries which are not well-connected to the international financial system.

And the sanctions that are being deployed against Russia are firstly, a form of financial warfare, not economic warfare (which would have more emphasis on trade restrictions).

The Financial Times (not paywalled) summarised it like this:

In recent years, Washington has often furthered its foreign policy through what’s referred to as the “weaponisation of finance”. What that has meant in practice is using the dollar’s global dominance to cut the monetary authorities of Iran, Venezuela, and (most recently and very controversially) Afghanistan off from access to their own reserves.

But the difference is that Russia is a much larger economy, and although it had taken steps in recent years to shield itself against such “weaponisation”.

Nonetheless, the financial sanctions appear to have had the intended effect. There are useful pieces by both Adam Tooze and James Meadway on different aspects of this.

Tooze first, noting that the ruble had falled, and the central bank had been required to hike interest rates to 20%, halt trading on the Moscow Stock Exchange, and impose stringent currency controls:

The collapse of the Russian currency may have deep political implications. As Ben Judah put it, the current collapse to him was reminiscent of the

“… worst day of the 1998 collapse. Gleb Pavlovsky once told me the default that followed was the “second founding of the state.” I am certain the crash we are about to see will in many ways come to be the third.”

The Kremlin is not in denial about their effects:

The critical issues here is that the sanctions have also been imposed on the Russian Central Bank. This means that although Russia has built up substantial reserves against financial sanctions, a lot of these funds are no longer accessible to them, because the central bank can’t move them.

Tooze’s piece is a little technical, though not impenetrably so. There’s an important point here, though. What’s new here is including the Central Bank in the sanctions, which apparently didn’t happen in 2014, after the incursion into Donbass.

The crucial thing is that reserves of euros and dollars can be put to work only by selling them in western financial markets. Those transactions require intermediary banks. And those banks can be blocked from engaging in transactions involving Russia’s central bank. To do this to a fellow central bank involves breaking the assumption of sovereign equality and the common interest in upholding the rights to property. It is a major step not easily taken against a central bank as important and as much part of the Western networks as the central bank of Russia.

There’s a lot more here, but quite a big question, because balance sheets always have two sides. If those Russian reserves are Russian assets, whose liabilities are they? Where else are they sitting on the global balance sheet? There could be a financial shock for the West—simply because of the scale of the assets involved. It may be that the delay in agreeing on the scale of these financial sanctions at the end of last week was while they worked out a plan to buffer against these potential shocks.

James Meadway adds some explanation to this, and some striking history.

The first is about SWIFT, the bank payments mechanism that Russia has now been excluded from:

SWIFT... facilitates the more rapid request of money transfers between international banks, and therefore facilitates foreign trade. It is not essential to foreign trade: banks in different countries can request money off each other in different ways if they are denied access to it, even if that has to be via fax. Since 2014, after the US first threatened to pull the plug on Russian access to SWIFT, the country has been busily setting up its own interbank communications system, SPFS, operational since 2017.

In fact, Russia is not the only country to have developed an alternative system. China has too, and so has India. So one effect of the use of financial weapons is likely to be the decline of financial globalisation and the strengthening of regional trading blocs. But that all takes time, and in terms of the sanctions, what matters is the immediate short-term. Attacking a central bank has much less risk to the West than sanctions on oil or gas or destabilising the banking system more widely:

There is, however, an economic weapon that can be utilised at no economic cost to those wielding it. A bank run in Moscow costs Berlin, London or Washington nothing. And so the primary weapon of the sanctions package are the restrictions on Russia’s central bank. The joint communique says:

“we commit to imposing restrictive measures that will prevent the Russian Central Bank from deploying its international reserves in ways that undermine the impact of our sanctions.”

And in turn that weakens the domestic financial system within Russia:

If Bank of Russia cannot sell its reserves, with institutions holding its assets unwilling to offload them, and others unwilling to buy them, the operation to prop up the rouble becomes impossible. The rouble will collapse, as we have seen this morning. That, in turn, threatens a bank run, as depositors look to remove their increasingly worthless roubles from bank accounts, and turn them into more valuable and stable currencies – like the dollar or the euro.

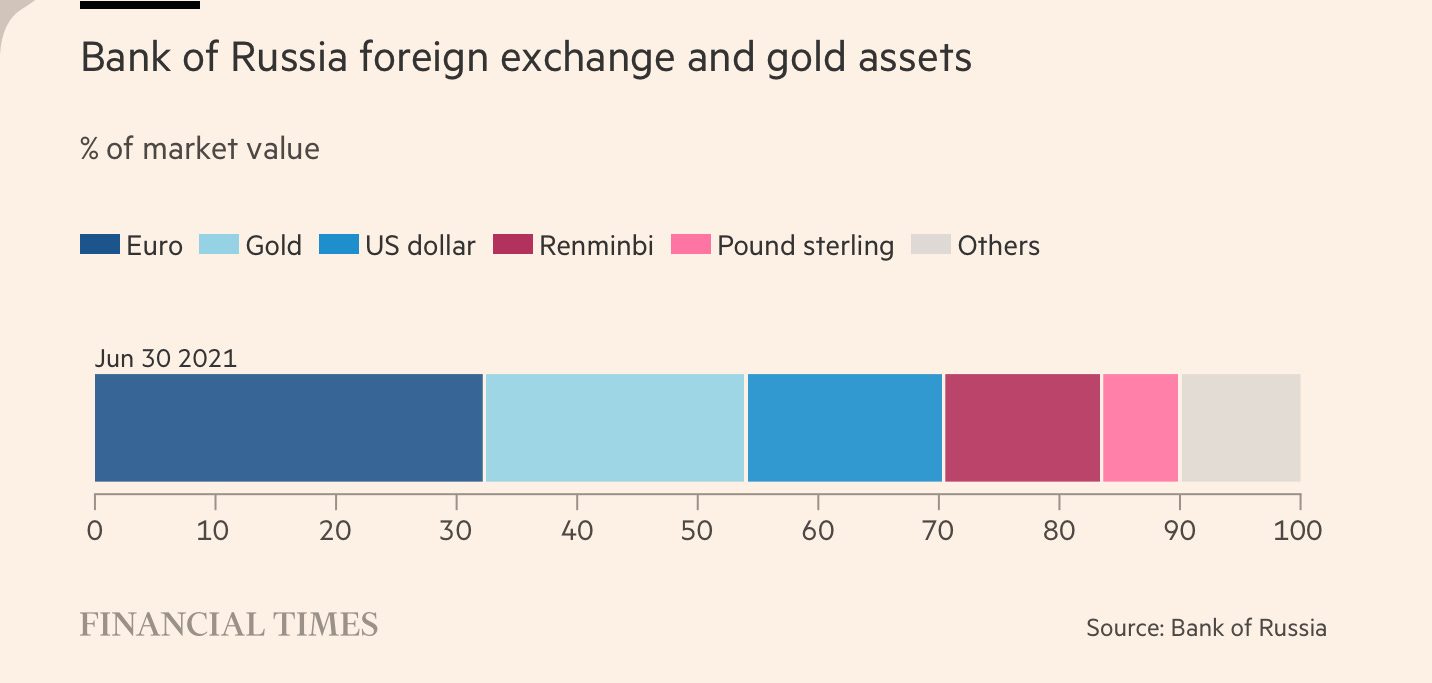

As Meadway notes, with a little help from a chart from the Financial Times, this only affects some of the bank’s reserves. It holds gold and renminbi, for example, and has “swap lines” open with China that it might draw on. (Although, as Meadway says, the Chinese might not be so keen on this).

Meadway also asks how governments learnt to deploy this power against central banks. And, he argues, it emerged in the wake of the financial crisis as a way to discipline economies that were not behaving as asked, notably in the Eurozone.

Documents leaked in November 2014 showed that the European Central Bank threatened the Irish government with the collapse of its banking system if it did not accept the ECB/EU/IMF bailout four years earlier. Even more dramatically, the ECB repeatedly threatened to end emergency support for Greece’s insolvent banks if the newly-elected Syriza government did not accept the bailout conditions it was offered from February 2015 onwards.

Meadway has a relatively radical view of political economy, and it’s possible that there are other interpretations out there.

But there is an important difference: Ireland and Greece were both part of an economic alliance, and therefore were going to negotiate and eventually comply. Meadway wonders whether the escalation of Russian rhetoric to include nuclear weaponry was partly prompted by its awareness of how brutal financial warfare could be. And: it will still hit the poor harder than the rich.

2: During the war. Reading Ilya Kaminsky

As regular readers know, sometimes there are different ways of saying things. Ilya Kaminsky is an American poet who was born in Odessa, whose family was granted asylum by the United States when he was in his teens. His poem sequence, Deaf Republic, was published in 2019.

Here are two poems from the book—copyright Ilya Kaminska, of course. Despite Substack’s ‘poetry block’ feature, it still doesn’t handle poetry very well, and can’t be previewed, so I’m hoping that spacing and line breaks are reasonably close to the original.

We lived happily during the war

by Ilya Kaminsky

And when they bombed other people's houses, we

protested

but not enough, we opposed them but not

enough. I was

in my bed, around my bed America

was falling: invisible house by invisible house by invisible house-

I took a chair outside and watched the sun.

In the sixth month

of a disastrous reign in the house of money

in the street of money in the city of money in the country of money,

our great country of money, we (forgive us)

lived happily during the war.

In a Time of Peace

Inhabitant of earth for fortysomething years

I once found myself in a peaceful country. I watch neighbors open

their phones to watch

a cop demanding a man’s driver’s license. When a man reaches for his wallet, the cop

shoots. Into the car window. Shoots.

It is a peaceful country.

We pocket our phones and go.

To the dentist,

to buy shampoo,

pick up the children from school,

get basil.

Ours is a country in which a boy shot by police lies on the pavement

for hours.

We see in his open mouth

the nakedness

of the whole nation.

We watch. Watch

others watch.

The body of a boy lies on the pavement exactly like the body of a boy.

It is a peaceful country.

And it clips our citizens’ bodies

effortlessly, the way the President’s wife trims her toenails.

All of us

still have to do the hard work of dentist appointments,

of remembering to make

a summer salad: basil, tomatoes, it is a joy, tomatoes, add a little salt.

This is a time of peace.

I do not hear gunshots,

but watch birds splash over the backyards of the suburbs. How bright is the sky

as the avenue spins on its axis.

How bright is the sky (forgive me) how bright.

from Deaf Republic

Ilya Kaminsky’s website is here, with links to more of his work. Or just buy the book. .

Other notes

It’s World Futures Day today—a round the clock set of talks and event that started a few hours ago in New Zealand. It’s hosted by the Millennium Project, and access is free. There’s more information here.

j2t#271

If you are enjoying Just Two Things, please do send it on to a friend or colleague.